The world has changed, and family offices are shifting their investment focus in response to a heightened geopolitical and financial risk. That’s among the findings in the 2026 Global Family Office Report released today by UBS, the Switzerland-based financial services giant that manages nearly US$5 trillion worldwide.

The 2026 study—based on interviews with more than 300 UBS single-family office clients, managing an average of US$1.7 billion in assets—also points to challenges beyond financial management, including governance and succession planning.

The UBS report is global in scope, including responses from more than 50 jurisdictions, and it does not break out Canadian responses. But it does point to important trends among SFOs that are relevant to the Canadian family office landscape.

Shifting allocations in response to new risks

As stewards of wealth, family offices have garnered a reputation as stable, patient allocators with a long-term investment horizon. Radical changes in investments are typically rare. In previous UBS surveys, for example, only about one-quarter to one-third of respondents said that they were planning to change asset allocations over the following year.

This year’s study suggests that the ground is shifting, and family offices are responding. The UBS survey found that 61 per cent of SFOs are concerned about a major geopolitical conflict over the next five years; more than half (56 per cent) are worried about a significant debt crisis over the same time frame. “This longer-term framing distinguishes today’s risk environment from more cyclical episodes of stress,” the report notes, “and appears to be informing how family offices approach portfolio construction and oversight.”

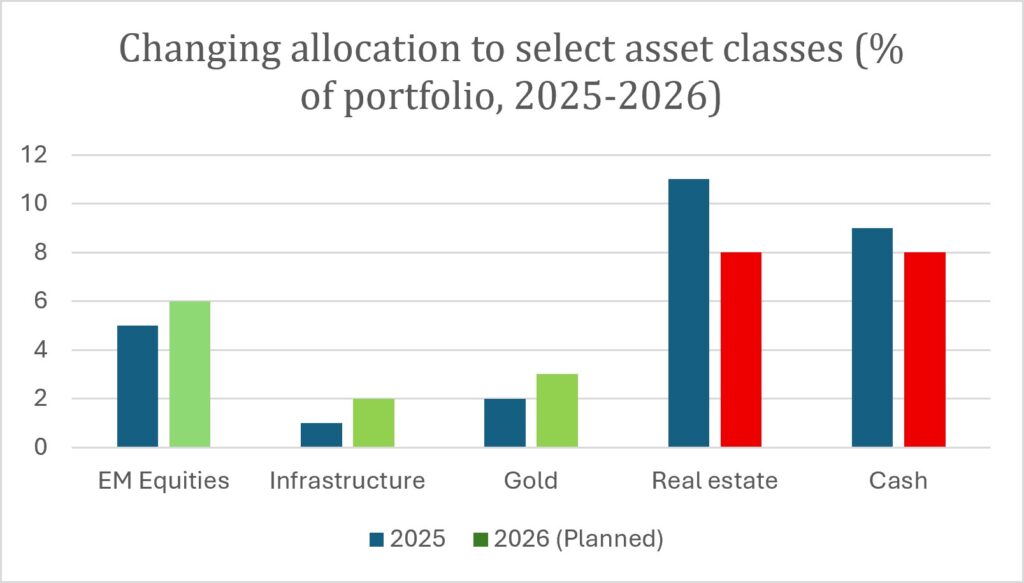

More than half of family offices—60 per cent—reported that they plan to change asset allocations over the next 12 months. Emerging market equities, gold and infrastructure are among the classes poised to attract more investment; real estate, meanwhile, seems set for a reduction in investment, perhaps reflecting expectations for continuing higher interest rates. While the planned changes are small, the report characterizes them as signs of “deliberate recalibration, as family offices adjust long-term positioning in response to a changing environment.”

Declining confidence in the greenback

Family offices are shifting not only what they are investing in, but where they are investing it. Part of that shift is driven by weakening confidence in the U.S. dollar’s traditional status as the world’s reserve currency. Nearly two-thirds of family offices expect confidence in the greenback to decline over the next 12 months. Almost 30 per cent have already reduced or are considering reducing their USD exposure, and 47 per cent said that they still consider themselves over-exposed to the greenback, compared with only seven per cent over-exposed to the euro (and only four per cent to the Canadian dollar). About a third of family offices in the survey said they have already increased or are considering increasing diversification across multiple currencies.

Canadian Family Offices Newsletter

Never miss an update! Subscribe to our newsletter and get new content straight to your inbox.

By clicking on the sign-up button, you consent to receive the above newsletters from NarrowContent Networks Ltd. You may unsubscribe any time by clicking on the unsubscribe link at the bottom of our emails or any newsletter. NarrowContent Networks Ltd | 100 York Blvd Suite 550, Richmond Hill, ON L4B 1J8 | info@canadianfamilyoffices.com

Outside the U.S., looking beyond the U.S.

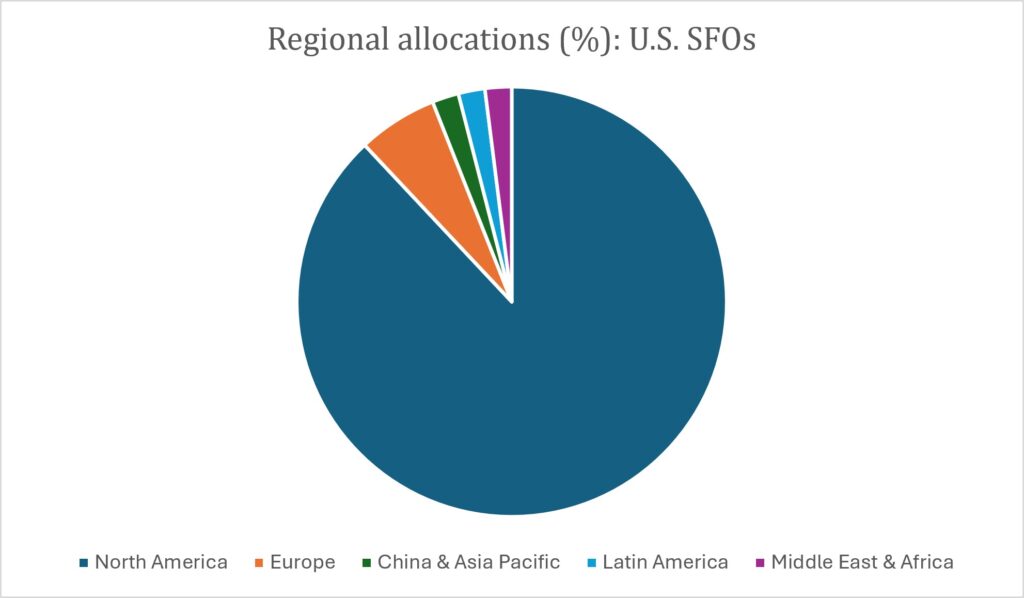

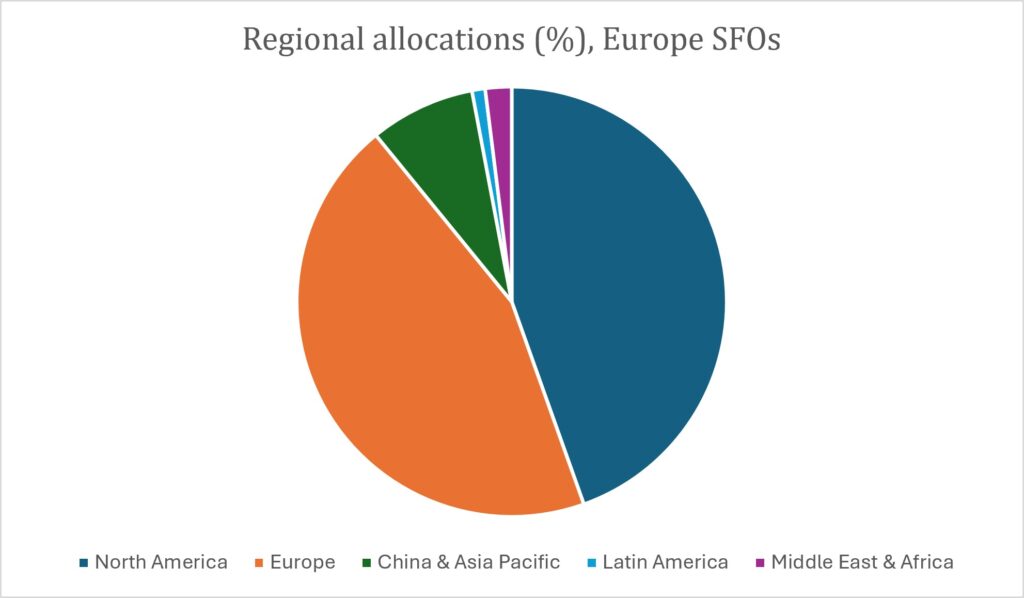

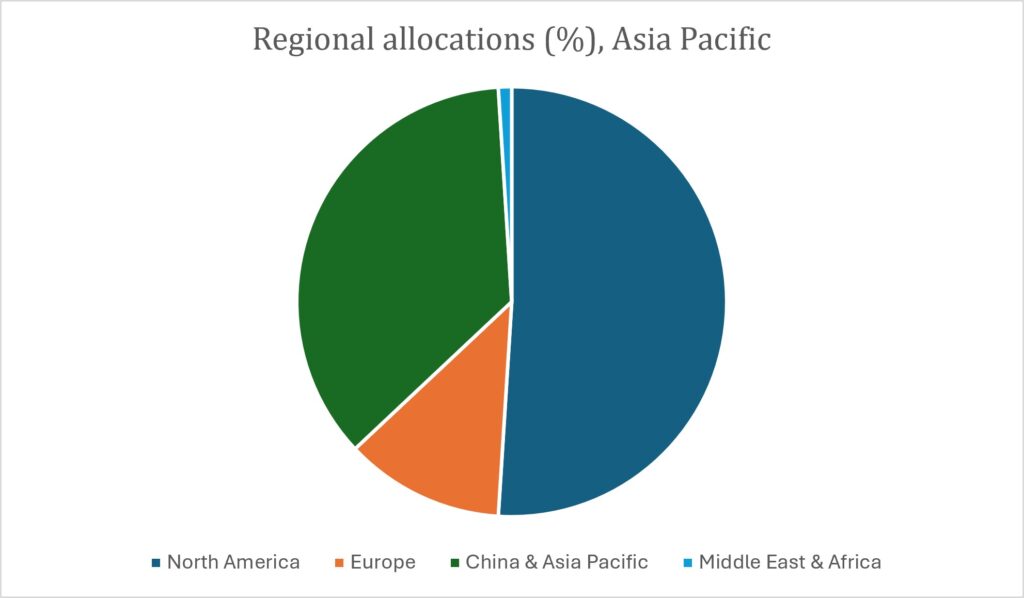

Globally, North American (largely U.S.) assets continue to dominate family office portfolios, attracting 52 per cent of planned allocations in 2026 across all respondents to the UBS survey. But home bias among U.S. family offices skews that finding, and elsewhere in the world there is more interest in non-U.S. allocations.

While U.S. SFOs say that North American assets comprise a formidable 88 per cent of their portfolio allocations—up from 86 per cent last year—it’s a different story in Europe (45 per cent North America allocation) and Asia Pacific (51 per cent). In those two areas, family offices are increasingly looking to “rebalance regional exposure,” the report notes, and “interest is growing in Asia Pacific, including Greater China, alongside Western Europe.”

Alternatives at the core, AI on the rise

For family offices, alternative assets continue to play a significant role in portfolio allocations. According to UBS, alternatives comprised 42 per cent of portfolios in 2025, down slightly from 44 per cent in 2024. (Public equity and fixed income comprised 58 per cent of allocations, including cash at nine per cent.) Among alternatives, private equity (17 per cent) and real estate (11 per cent) were the most widely held classes, followed by hedge funds (six per cent) and private debt, which comprised just three per cent of allocations.

Interestingly, more than a third of SFOs said that they are considering increasing exposure to hedge funds over the next five years.

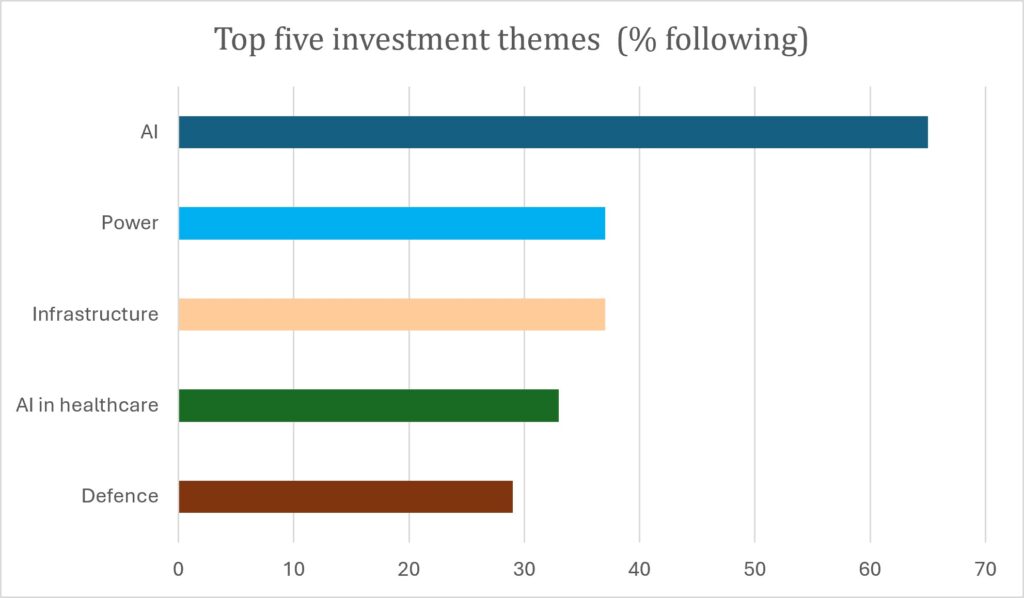

The UBS report further asked respondents about investment themes they follow to guide allocations. The leading theme is perhaps no surprise: artificial intelligence. The survey found that 65 per cent of SFOs are invested in AI, with interest “strongest in areas closely linked to the build-out that supports wider adoption, including data center infrastructure, software platforms, and semiconductor producers.” There was also significant conviction in other themes, including power generation (probably related to the AI buildout and its energy demands), infrastructure, AI in healthcare, and defence and security infrastructure.

Governance gaps, transition uncertainty

Outside of asset allocations and investment strategy, the UBS survey also asked SFOs about their services, operations and governance practices, providing some illuminating insights into how family offices actually work around the world.

When it comes to service provision, the survey found that investment functions are largely administered internally; a clear majority provide asset allocation (86 per cent) and portfolio risk management (80 per cent) in-house. Meanwhile, most SFOs say they also handle succession planning and preparation of the next generation internally. In contrast, legal services, tax planning, cybersecurity and lifestyle (concierge) services are mostly outsourced.

On governance, UBS notes that formal processes “are now a common feature of family office operations,” but that governance practices “are not applied uniformly across all dimensions of the family office.” Reflecting the importance of investment management as a core function, most SFOs have formal processes for measuring financial performance and 60 per cent have an investment committee. However, non-investment functions receive weaker governance focus. Only about 40 per cent have cybersecurity controls; fewer have a succession plan for the family office to ensure continuity of staff and operations (35 per cent) or a risk management process beyond investments (28 per cent), for instance for reputation, health or property.

Another governance gap: only about one quarter of SFOs have an organized framework for preparing the next generation for their future responsibilities. Clearly, transition planning and education for the next-gen remain an area of opportunity for many SFOs, and so is developing strategies for more actively involving younger generations in the family office.

In the study, 45 per cent of SFOs surveyed said that the next generation is fully or partially involved in the family office. (An additional 32 per cent said that the next gen were too young to be involved.) However, 21 per cent overall agreed that the next generation “has no involvement in the family office but is old enough to participate.” To reframe that finding: the next gen has no family office involvement—are “still on the sidelines,” as UBS puts it—more than 30 per cent of the time even when they are not too young.

Why the gap? UBS suggests the barriers to the next generation “are not just age-related, but reflect perceived differences in priorities between generations, alongside gaps in financial education.” On the plus side, the report notes that more than half of SFOs where the next gen has limited involvement are planning to introduce education programs, while others are looking to get them involved in philanthropy, entrepreneurial ventures or investment committees.

The UBS Global Family Office Report 2026 contains regional insights and other findings of potential interest to the family office community. To download a copy (registration required), click here.

Joe Chidley is managing editor of Canadian Family Offices.

The Canadian Family Offices newsletter comes out on Sundays and Wednesdays. If you are interested in stories about Canadian enterprising families, family offices and the professionals who work with them, but like your content aggregated, you can sign up for our free newsletter here.

Please visit here to see information about our standards of journalistic excellence.