A third time might not be the charm in this instance, but one of the nation’s leading wealth managers for some of Canada’s wealthiest investors is once more raising concerns about historically high valuations in the United States’ equity market.

“I’m ringing that warning bell a third time to really emphasize caution about how stretched U.S. market valuations have become,” says Thane Stenner, founder of Stenner Wealth Partners+ at CG Wealth Management and Chairman Emeritus of ultra-high-net worth (UHNW) network Tiger 21 in Canada.

He previously held award-winning consulting roles at Morgan Stanley/Graystone Consulting, while based in California as Managing Director, International Client Advisor, Institutional Consulting Director, Alternative Investments Director and Portfolio Manager. He also hosts “Smart WealthTM with Thane Stenner,” a podcast produced by BNN Bloomberg Brand Studio.

In previous Canadian Family Offices articles, February 19, 2025 (right before a 20-28 per cent sell off in S&P 500 + NASDAQ, respectively) and October 14, 2025, Stenner discussed how the U.S. stock market’s valuations are higher than prior to the dot-com crash and the 1929 one that sparked the Great Depression. For this piece, Stenner’s quotes were taken as of February 2, 2026.

Indeed, after the first warning, markets did dip dramatically (20-28 per cent) from February 20, 2025 to early April after U.S. President Donald Trump announced across the board tariffs. That downturn was short-lived. Stenner says his investment team took advantage of the dip to opportunistically buy back into the market at lower prices.

“The markets since have been pretty strong and have achieved an all-time high as of today, January 27, 2026.”

His team’s discretionary model global ETF portfolio returned more than 23.2 per cent in 2025, beating the NASDAQ and S&P 500 handily in Canadian dollar terms. Yet in 2026, his team moved to a very defensive stance of 60 per cent cash and does not use any leverage (as of today, January 27th/26), along with hedged positions to prepare to take advantage of a potential looming market correction.

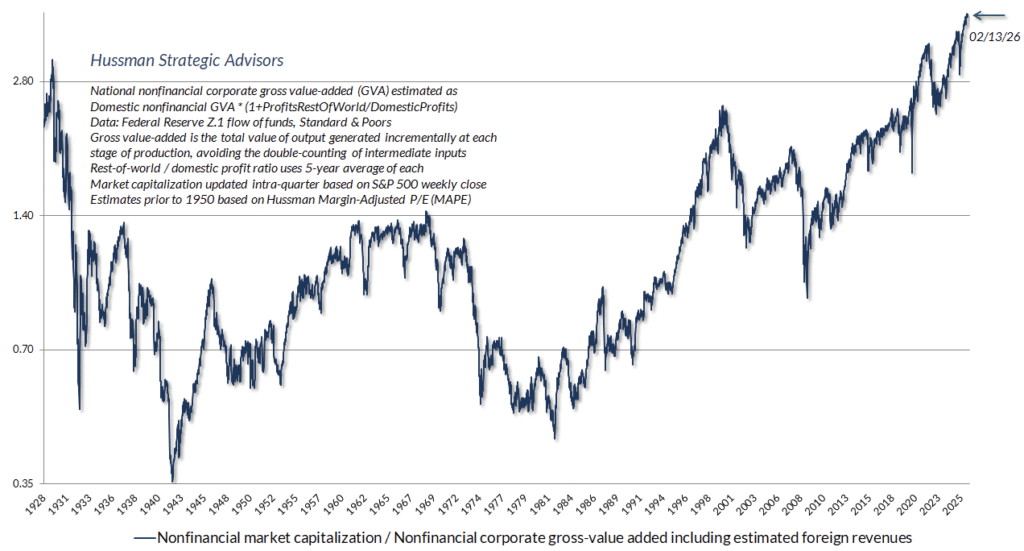

As he did in the previous articles, Stenner points to a handful of charts, including one previously featured in one of those pieces: Hussman Strategic Advisors’ proprietary margin-adjusted price to earnings ratio.

“It’s like a compilation of a few valuation ratios, and it’s one that Warren Buffett has said is the best he’s ever seen for representing total market valuations,” Stenner says.

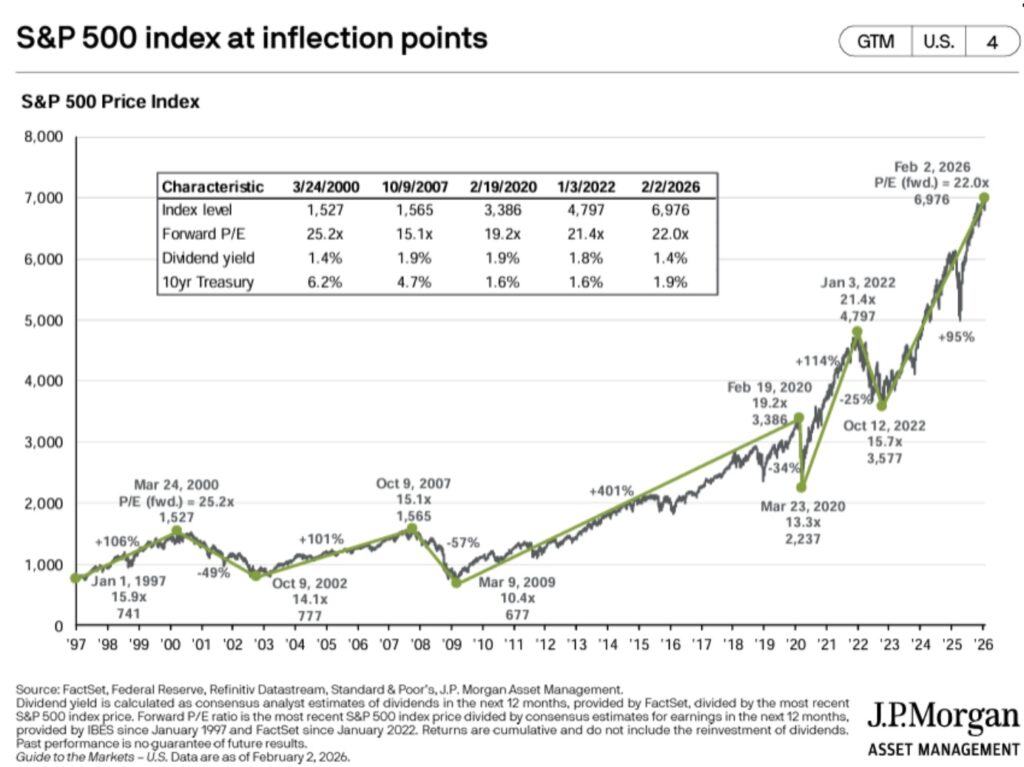

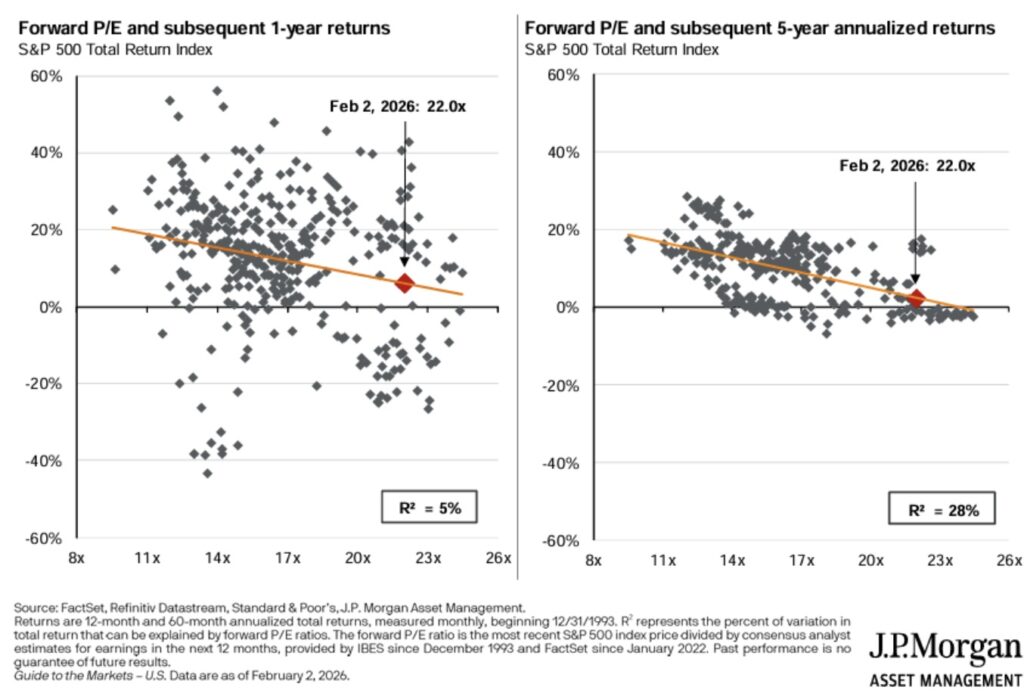

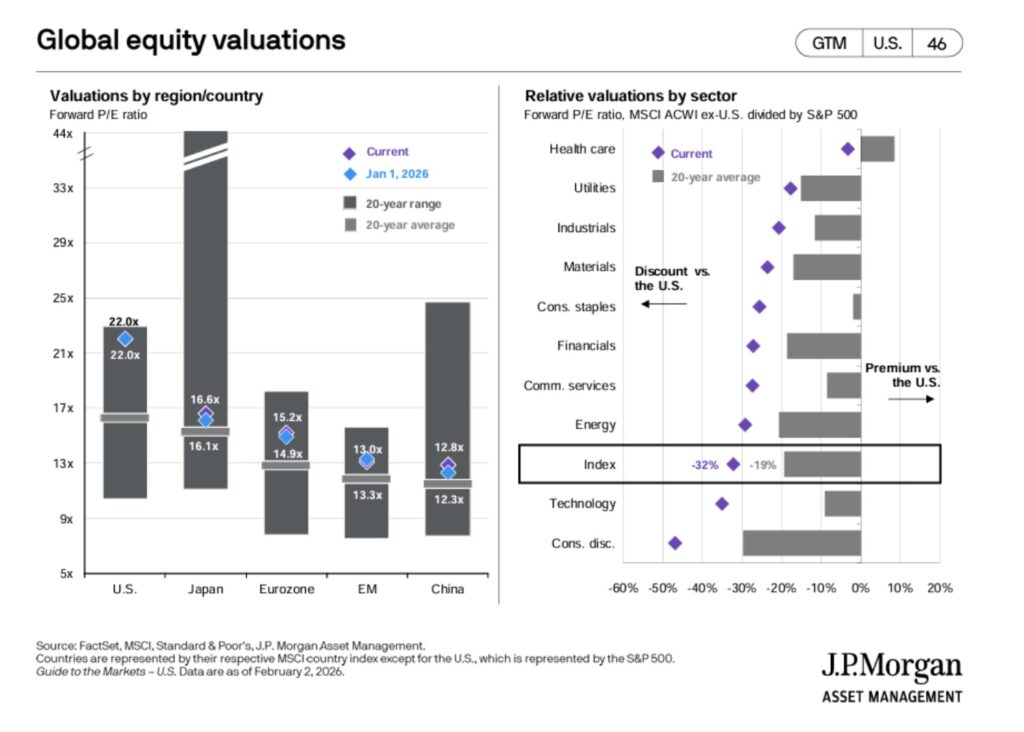

Stretching from 1928 to Dec. 26, 2025, it illustrates how the S&P 500—the world’s largest stock index by market capitalization—is at its highest valuation in almost 100 years.

Notably, in every other period where this metric reached historical highs, a market plunge followed. “The probabilities of at least a meaningful correction, if not a full-blown bear market, at some point in the next six to 24 months are really high,” Stenner says.

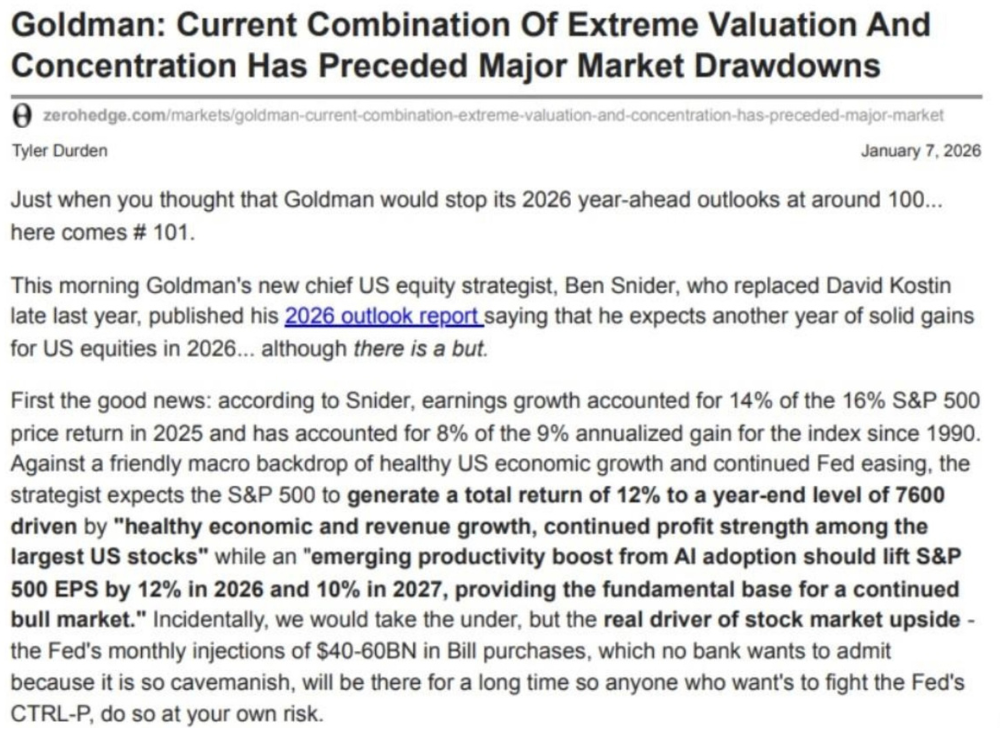

Valuations and profits are highly concentrated among a few stocks.

I’m ringing that warning bell a third time to really emphasize caution about how stretched US Market valuations have become.

Thane Stenner

Top 10 stocks

“Right now, the top 10 names in the S&P 500 make up about 40 per cent of the market value,” he adds, pointing to a recent report from Zero Hedge digging into a Goldman Sachs analyst’s assessment of the U.S. market.

Those top 10 stocks—which are mostly big tech, including the so-called Magnificent Seven—also made up 53 per cent of the return last year on the U.S. market.

The report further notes that the market’s current position “rhymes with a handful of overextended equity markets in the last 100 years.”

Those include the 1920 “Roaring 20’s” boom, the “Nifty Fifty” dominance in the early 1970s, and the 1987 bull market before Black Monday. That’s not even including the run-ups to the dot.com crash and in 2021 before the 2022 correction.

Boom dot-com?

The market indeed shares some similarities to the dot-com era, Stenner says. At the time, investors were euphoric about the Internet’s promise, he recalls.

“We made a lot of money the prior seven years (leading up to the early 2000s) for clients, but we rotated out of the broad equity market—especially technology—and invested in beaten-up REITs and resources that were significantly neglected and undervalued then,” he adds.

That did not sit well with some clients. “But we stuck to our guns and rotated to those two sectors, which were down 45 to 50 per cent the prior five years. Both these undervalued sectors soared hard the following 5 years.”

It took a few months for the thesis to bear fruit, as the NASDAQ went up another 20 per cent. “I had lots of egg on my face during that brief, few months period.”

Eventually, though, the bubble burst, and the NASDAQ plunged 89 per cent from exact peak to low point over the next two and a half years.

Stenner notes that his investment team doesn’t attempt to time the market, but they do pay attention to stretched valuations and take profits/use hedges to protect investor capital.

Past aging bull runs

Similar to past aging bull runs, today he frequently hears “this time is different” and how we have entered “a new era of higher valuations” because of the massive potential for profitability from artificial intelligence.

You often hear that type of discussion before a big unravelling of markets.

Thane Stenner

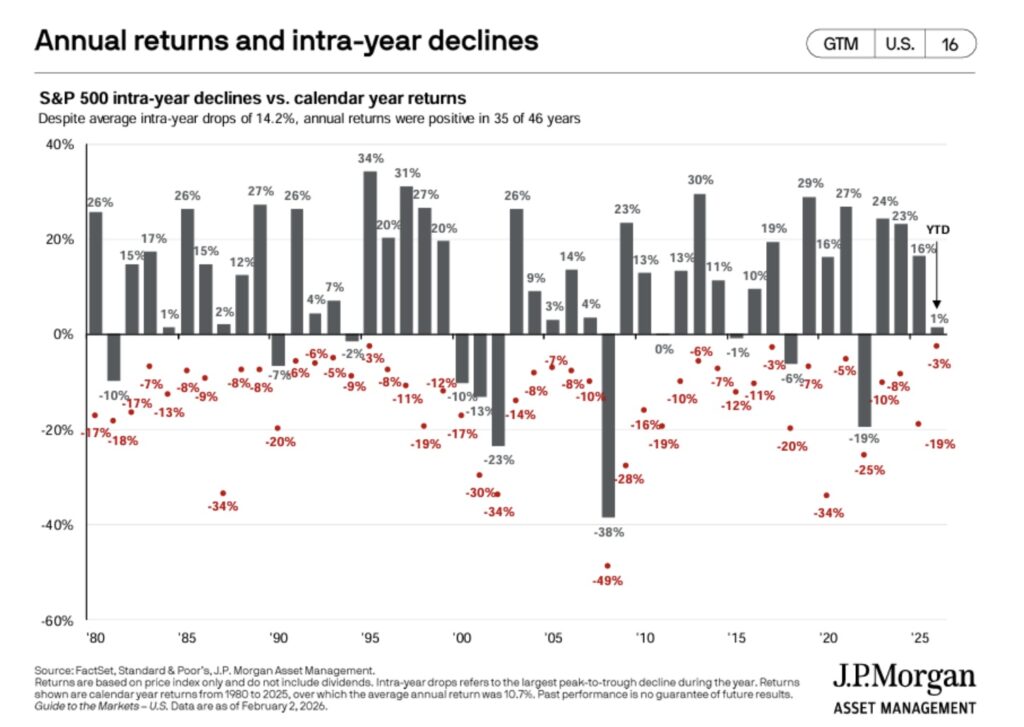

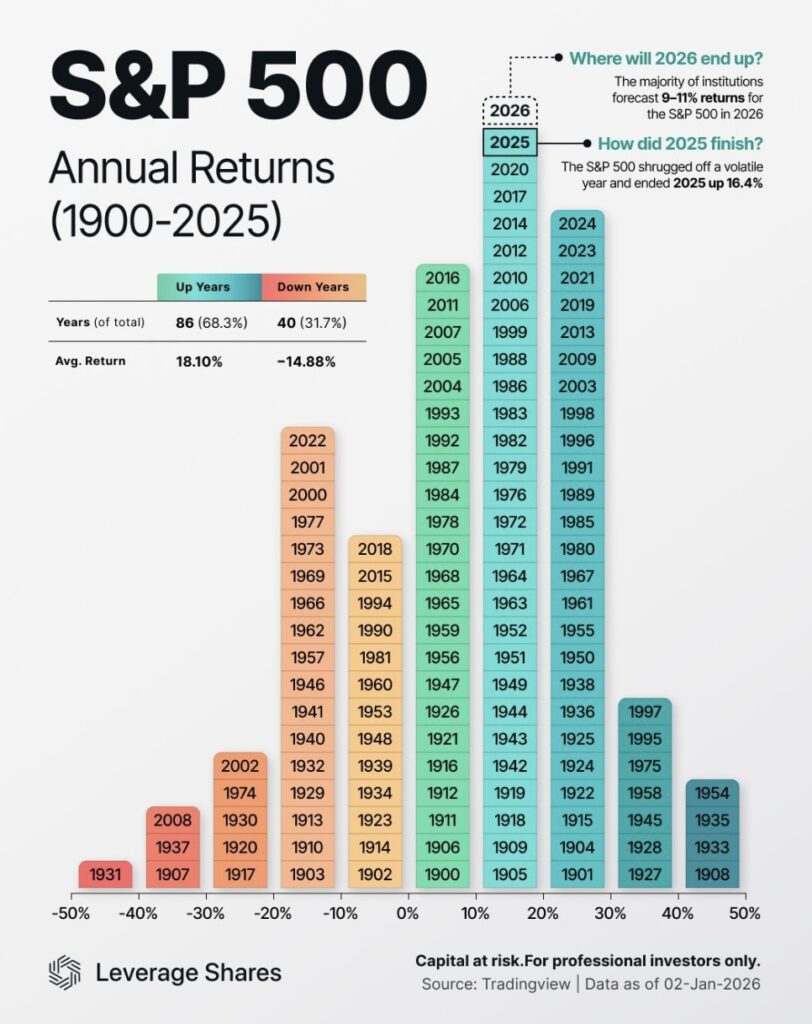

Stenner further points to another chart showing percentage losses and gains in the U.S. stock market for the last 126 years. It shows that 86 (68.25% of the time) of those years had positive returns. Among those, 40 that weren’t positive were 1929, 1930, 1931 and 1932–and the cumulative decline would have taken investors in 1929 25 years to recover their losses.

History may not repeat itself perfectly, and the AI revolution indeed has enormous potential to drive profitability. But current valuation risks are difficult to ignore, Stenner cautions. Among them are circular funding models among big tech like the recent $100-billion deal whereby chipmaker Nvidia will invest in OpenAI to help build data centres. Inevitably, that means the AI company will purchase Nvidia chips to be used in those facilities.

A historical conclusion

Other risks are geopolitical, notably a dramatic shift from globalism to regionalism led by the U.S. Here, Stenner points to the work of historian Neil Howe, co-author of The Fourth Turning: What the Cycles of History Tell Us About America’s Next Rendezvous with Destiny.

Howe writes about how the U.S. goes through repeating historical phases, with the “fourth turning” being one of extreme upheaval. Many observers of his work believe we are now already in that part of the cycle, Stenner says.

“We’re in the early days of a ‘winter phase,’” he adds, pointing to Howe’s terminology to describe this period of high volatility.

That’s not to say opportunities to invest profitably won’t emerge.

“Investors with nimble strategies who can be tactical are going to find great opportunities in 2026 and 2027,” Stenner says.

“But for large investors like family offices, the goal today should be protecting capital first and foremost and, second, being positioned to seize opportunities that will arise from the coming volatility.”

*Responses have been lightly edited for clarity and length. Mr. Stenner’s viewpoints within this interview were submitted to CFO on February 2nd, 2026.

Follow Thane Stenner and Stenner Wealth Partners+ on LinkedIn.

Thane Stenner Interviews/Articles, Member of Canadian Family Offices.

About Stenner Wealth Partners+

Stenner Wealth Partners+ (SWP+) is an in person/virtual Multi-Family Office/Outsourced CIO Consulting team of financial/wealth specialists with a boutique approach and global perspective. SWP+ serves Canadian and US investors/households with generally a minimum of 10M+ in investable assets or 25M+ net worth. As a CG Wealth Management team, SWP+ is a highly exclusive practice team with one of Canada’s largest independent wealth management firms. Client Range of Net Worths: between $25M To $3B+. They strategically limit new client engagements, onboarding only six to eight new key relationships annually to ensure a highly personalized and focused approach. SWP+ is a member of Canadian Family Offices.

About CG Wealth Management

The global wealth management business is entrusted with C$144.8 billion in client assets1. The wealth management operations of the Canaccord Genuity Group (CG Wealth Management) provide comprehensive wealth management solutions and brokerage services to individual investors, private clients, family offices, Donor Advised Funds (DAFs), and intermediaries through a full suite of services tailored to the needs of each client.

1Canaccord Genuity Annual Report, December 31, 2025

Disclaimer: This story was created by Canadian Family Offices’ commercial content division on behalf of Stenner Wealth Partners+ at CG Wealth Management, which is a member and content provider of this publication. CG Wealth Management is a division of Canaccord Genuity Corp., member of CIPF and CIRO. Tax & Estate advice offered through Canaccord Genuity Wealth & Estate Planning Services Ltd. Thane Stenner’s views, including any recommendations, expressed in this article are his own only, and are not necessarily those of Canaccord Genuity Corp.

Joel Schlesinger is a Winnipeg-based freelance writer who has written for Canadian Family Offices since 2021. Specializing in investment, wealth advice, real estate and personal finance, he is also a regular columnist for the Winnipeg Free Press, and his work regularly appears in The Globe and Mail, Calgary Herald and Edmonton Journal.