Most experts agree that enterprising families ought to lay out some guidelines regarding the business and how they interact with it. Yet a majority of them don’t have this kind of documented governance.

That’s according to the UBS Family Office survey for the first quarter of 2026, which found that 62 per cent of family offices globally don’t have formal governance structures. It means that if a crisis hits, the family and the business could implode, like the multi-generational, Hyatt Hotel-owning Pritzker family did earlier this century.

But what exactly is governance in a family office context, who is it for and how can it protect the family, its wealth and business?

As Canadian family offices move into their second, third and fourth generations, professionalization has become key to maintaining, growing and transferring wealth.

Governance does that by creating a framework for the processes, rules and structures that manage, preserve and transition wealth to the next generation. When done right, family members’ roles are clear, the decision-making process is laid out, and family harmony is maintained. Or, as Patricia Saputo, co-founder and strategic advisor at Crysalia, says, “It’s how decisions are made. Is there any established process of decision making?”

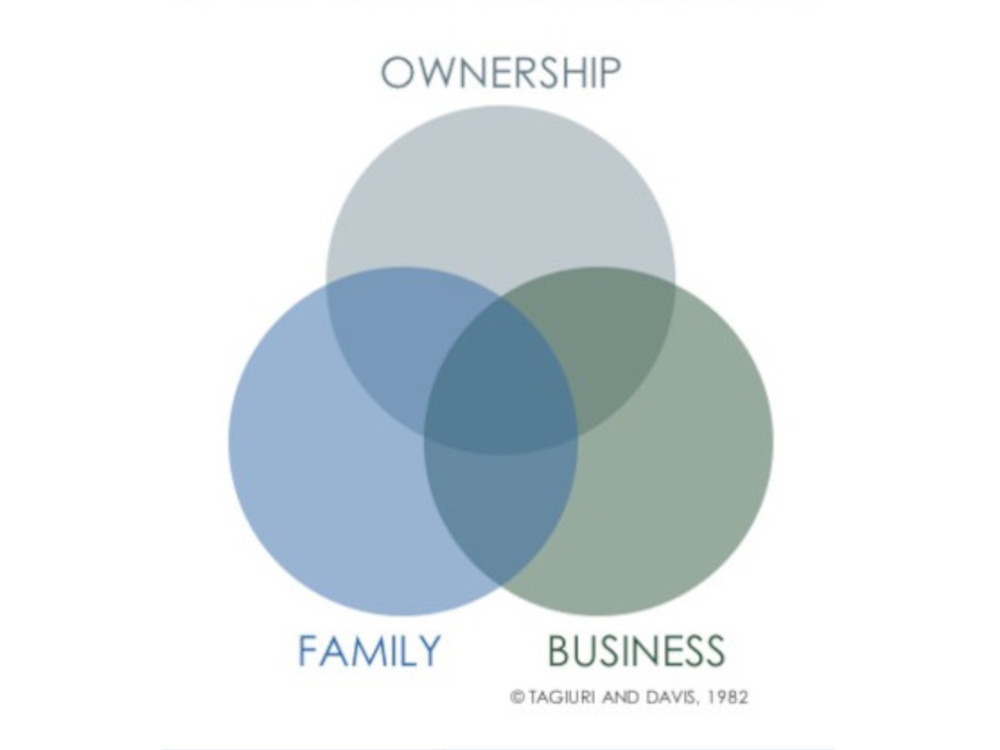

Governance applies to the three-circle model of family business, which was introduced in the 1980s by John A. Davis and Renato Tagiuri. The model reflects how the different stakeholders—family, business and ownership—are interdependent, and how a decision in one circle can affect the others. One example is whether spouses are allowed to work in the family business.

Chris Gandhu, partner and family office leader with KPMG Canada in Calgary, says that at a very high level, governance is about who makes a decision and what authority they have to make that decision.

The worst case scenario is that the family falls apart, and they all go get their own lawyers, and then it’s the lawyers fighting, and then the money goes to pay legal fees.

Patricia Saputo, co-founder and strategic advisor, Crysalia

“Because governance is more about the process than the document itself, it’s not sufficient to say, ‘Yeah, we developed a family constitution X number of years ago,” he says. “I would say you have to take it a step further. Governance truly exists and thrives when you’re practicing it, because conflict is inevitable.”

Then why do so many family offices neglect governance?

One reason, says Gregory Moore, partner with Richter Family Office in Toronto, is that the founding generation may not want to give up control. Another is that the family might find it overwhelming. And some believe that governance would stifle entrepreneurship.

“If you’re coming from an entrepreneurial environment, and it’s going from controlling generation to emerging generation, there is this perspective of not wanting to create a formal framework because that disincentivizes some of the core principles of being an entrepreneur—having the ability to make decisions on the fly and not having a management-by-committee type of approach,” Moore says.

But a lack of documented governance can result in negative outcomes, says Saputo.

“The worst case scenario is that the family falls apart, and they all go get their own lawyers, and then it’s the lawyers fighting, and then the money goes to pay legal fees,” she says. “And the family’s left with nothing, and the family is in turmoil, and nobody’s talking to anybody after they’ve lost everything.”

Other less dire consequences that can harm all three circles in the family business model include ad-hoc or on-the-fly investment strategies and decision making; asset mismanagement; a lack of clear roles within the family and business, which can harm family and staff morale; higher costs and inefficiencies, which affect a company’s earnings; and poor succession planning and the resulting infighting among families, members of the C-suite or both.

Gandhu says that exercising governance on the fly may work but can lead to default reliance on the founder if he or she is the one who solves the problem—instead of following the path set by agreed-upon governance. “By relying on the process that you’ve co-created as a family, you must follow those protocols,” he says.

Proper governance can cover all scenarios and ease the leadership transition between generations. All our experts said that the earlier a family office puts governance on paper, the better.

Moore says a simple entry point is to start with the nuclear family and articulate the values and beliefs that are important to them.

“Does it mean [something] as fundamental as, ‘We love each other, we want to continue to work together and respect each other?’” he says. “That’s a pretty good framework for starting to bolt on other things and other understandings. And if you collectively as a group can articulate and agree upon that and actually making sure that all stakeholders have some sort of input and consensus building around what [the family] stands for and what’s important to them, then that’s a really good starting point. And then everything else, by and large, will be influenced by that perspective.”

Once governance has been documented, it shouldn’t be shoved in a drawer or left to rot in “the cloud.” It’s a living document that should be reviewed at least once a year, says Saputo, especially as younger generations grow up and the prevailing culture changes as a result of immigration, for example.

“If it’s culture change, it’s not just a matter of bringing the governance document to the table,” she says. “It’s a matter of accepting what’s going on in the world. Will the family change that culture, or is that culture so embedded that they refuse to? Some families are very stringent on that.”

Renée Sylvestre-Williams has written for Canadian Family Offices for three years. She is a Toronto-based journalist and content strategist with more than 15 years covering personal finance, insurance, taxes and investment. She has written for the Toronto Star, the Globe and Mail, WealthSimple, MoneySense and The Walrus. She is a COPA winner, editor of The Budgette (a newsletter focused on finance for solo earners), and the author of the book The Singles Tax (January 2026).

The Canadian Family Offices newsletter comes out on Sundays and Wednesdays. If you are interested in stories about Canadian enterprising families, family offices and the professionals who work with them, sign up for our free newsletter here.

Please visit here to see information about our standards of journalistic excellence.